Building a startup is a marathon, not a sprint. It’s a game of resilience, sharp strategy, and a brutally honest understanding of the challenges ahead. It's far more than just a brilliant idea; it's about proving people actually want that idea, finding the ones who will pay for it, and then meticulously building a real business around it.

Confronting the Reality of Building a Startup

Before you even think about a business plan or start hitting up investors, you need to internalize the unfiltered truth of this journey. The glamorous stories of overnight success you read about? They're the exception, the lottery winners. For most of us, building a company from scratch is a grueling, lonely, and statistically improbable marathon.

I'm not saying this to scare you off. I'm saying it to arm you. Knowing the odds, and why they're stacked against you, is your very first strategic advantage.

The hard numbers don't lie: around 90% of startups fail. This isn't a new trend; it's a consistent reality. But the reasons aren't some big mystery. They're predictable and, more importantly, avoidable traps. A massive 34% of failures happen because of a lack of product-market fit. In plain English, they built something nobody was willing to pay for. Another 22% crash and burn because of bad marketing. If you're a first-time founder, the hill is even steeper. You can dig into these startup failure stats to see the full picture.

Why Most Startups Stumble Out of the Gate

Understanding why companies fail is the key to not becoming one of them. It's about recognizing that a cool idea is worthless without execution, real market demand, and a coherent plan to get it in front of people.

Too many aspiring founders fall in love with their solution before they ever truly fall in love with the problem. They'll spend months, sometimes years, perfecting a product in a vacuum, only to launch to the sound of crickets. This is the classic, tragic product-market fit dilemma. It's a mistake born from making assumptions instead of gathering evidence.

Your goal isn't just to build a product; it's to build a business. That means getting out of your comfort zone, the world of code and whiteboards, and into the messy, challenging world of sales, marketing, and customer feedback from day one.

Adopting a Founder's Mindset

So, how do you beat the odds and join that successful 10%? It all starts with your mindset. The founders who make it aren't just dreamers; they're relentless, reality-based problem-solvers. They become obsessed with their customers' pain, not their own clever solutions.

This shift in thinking has a direct impact on how you approach building your company:

- Embrace Frugality. Don't even think about chasing venture capital until you have a concept that's been validated with real customers. Many of the best companies started by bootstrapping, a path that forces incredible discipline and creativity.

- Prioritize Learning Over Being Right. Let me be clear: your initial assumptions are almost definitely wrong. Your job isn't to be a genius; it's to test those assumptions quickly and cheaply, then adapt based on what the market tells you.

- Build for a Niche. Stop trying to build a solution for "everyone." Find a small, specific group of people who feel a particular pain point more acutely than anyone else. Solve their problem better than anyone else, and you'll earn your first true fans.

By looking these harsh realities square in the eye, you can build a strategy that anticipates obstacles instead of being blindsided by them. The path is incredibly difficult, but it's not impossible for those who come prepared.

Turning Your Idea Into a Validated Business

A great idea feels like lightning in a bottle. It's exciting, but it’s not a business, not yet, anyway. Right now, it's just a hypothesis. The single most important thing you can do is get out of your own head and rigorously test that hypothesis before you spend a single dollar on development.

This is the validation phase. It’s where you separate a passion project from a potentially profitable company.

The whole point here is simple: confirm that a real group of people has a problem you can solve, and critically, that they’re willing to pay for your solution. This doesn't require a huge budget or an MBA. It just takes hustle, curiosity, and a willingness to be proven wrong.

Find the Pain Before You Build the Ointment

The classic founder mistake? Building a brilliant solution for a problem nobody actually has. It’s easy to fall in love with your own idea and just assume everyone else will feel the same way.

To avoid this trap, you need to become an expert on the problem.

Start by getting specific about who you think your customer is. "Small business owners" is way too broad. Is it florists drowning in inventory paperwork? Freelance photographers who need a better way to deliver client proofs? That level of detail is everything. Getting this right is so fundamental and will guide just about every decision you make from here on out.

Once you have a rough sketch of your customer, your job is to talk to them. And I don't mean pitching your idea. Your job is to listen.

Your mission isn't to sell a product; it's to understand a struggle. Ask open-ended questions about their day, their frustrations, and the workarounds they've already tried. Your idea shouldn't even come up in the first conversation.

Scrappy Ways to Test the Waters

You don't need to commission a massive market research study. You can start gathering incredibly valuable insights this week with a few cheap and simple methods.

- Surveys and Polls: Tools like Google Forms or even a simple LinkedIn poll can be powerful. Just make sure your questions are aimed at uncovering pain points, not just confirming your own biases.

- The "Smoke Test" Landing Page: This is a classic. Build a simple one-page website that sells the dream of the value your future product will offer. Add a signup form for a "waitlist" or "early access." Then, drive a little bit of targeted traffic to it. If people sign up, you've got your first piece of evidence that you're onto something.

- Dig Through Competitor Reviews: Find out who's already trying to solve a similar problem. Go straight to their customer reviews, especially the 1- and 2-star ones. Those complaints are a goldmine of unmet needs and clues on how you can do it better.

A Real-World Validation Story

Let's walk through an example. A founder, Alex, has an idea for an app that connects homeowners with pre-vetted, on-demand local gardeners.

Instead of immediately hiring developers, Alex builds a simple landing page. The headline reads: "Get a trusted, local gardener to your door in hours." She includes a simple form to "Book Your First Service."

Next, she spends $100 on targeted Facebook ads aimed at homeowners in a specific suburb who have shown interest in gardening. Her goal isn't to make money; it's purely to see if anyone will bite.

After a week, 15 people try to book. Of course, there's no app. So Alex personally emails each one, apologizes for the "technical glitch," and offers them a discount for a future service. But here's the crucial part: she asks if they’d be willing to hop on a 15-minute call to talk about their gardening needs.

Through those calls, Alex discovers her initial assumption was a little off. People didn't just want an on-demand service for one-off jobs. Their real pain was finding someone reliable for ongoing, weekly maintenance.

This single insight is priceless. She just validated the core problem and uncovered a much more valuable, recurring-revenue business model. All of this happened before writing a single line of code. That's how you build a startup on a foundation of evidence, not assumptions.

Crafting a Minimum Viable Product That Works

So, your idea has legs. You've validated it, and you're confident you're onto something. Now comes the exciting (and dangerous) part: building it. This is the stage where many first-time founders go off the rails, pouring months of time and cash into building the "perfect" product.

That's a classic, fatal mistake. The goal right now isn't perfection; it's learning. And the fastest way to learn is to get a real product into the hands of real users by launching a Minimum Viable Product (MVP).

Let's be clear: an MVP isn't just a buggy, half-baked prototype. It’s the simplest, most focused version of your solution that solves one core problem for a very specific type of user. Think of it as your first real conversation with the market, one that uses a working product, not just a landing page, as the medium.

The Art of Ruthless Prioritization

The biggest threat to your MVP is "scope creep", the seductive whisper of "just one more feature" before you launch. This is where you have to be disciplined. You need a framework to separate the essentials from the fluff.

A tried-and-true method for this is MoSCoW, which helps you sort every potential feature into four distinct categories:

- Must-have: The absolute non-negotiables. The product is broken or useless without them. For a meal-planning app, this would be the ability to search for recipes.

- Should-have: These are important and add a lot of value, but the product can launch without them. Think of a feature to save favorite recipes.

- Could-have: The "nice-to-haves." They're cool, but they don't solve the core problem and can easily wait. A dark mode setting is a perfect example.

- Won't-have (for now): Features you consciously decide to push to a later release. Defining what you're not building is just as crucial as defining what you are. A complex social sharing integration would fit here.

This kind of framework forces you out of a vague "wouldn't it be cool if…" mindset and into a sharp, strategic approach. You're aiming to launch with only the "must-haves" so you can start getting that critical user feedback as fast as possible.

To help visualize this, I've put together a simple table that shows how to think about feature prioritization for an MVP.

MVP Feature Prioritization Framework

| Priority Level | Description | Example Feature (for a meal planning app) |

|---|---|---|

| 1: Must-Have | Absolutely critical for the product to function and solve the user's primary problem. Non-negotiable for launch. | User can search for recipes by ingredient. |

| 2: Should-Have | Important features that add significant value but are not essential for the initial release. | User can create a weekly meal plan and generate a shopping list. |

| 3: Could-Have | Desirable "nice-to-have" features that improve the experience but have a low impact on the core functionality. | User can filter recipes by dietary restrictions (e.g., vegan, gluten-free). |

| 4: Won't-Have | Features that are explicitly out of scope for the MVP. They might be built later, but not now. | Integration with grocery delivery services. |

Using a structure like this ensures your entire team is aligned on what truly matters for day one.

The MVP is about finding that sweet spot between "minimum" and "viable." It needs to be polished enough to solve a real problem and earn a user's trust, but lean enough that you don't burn through your resources building something nobody wants.

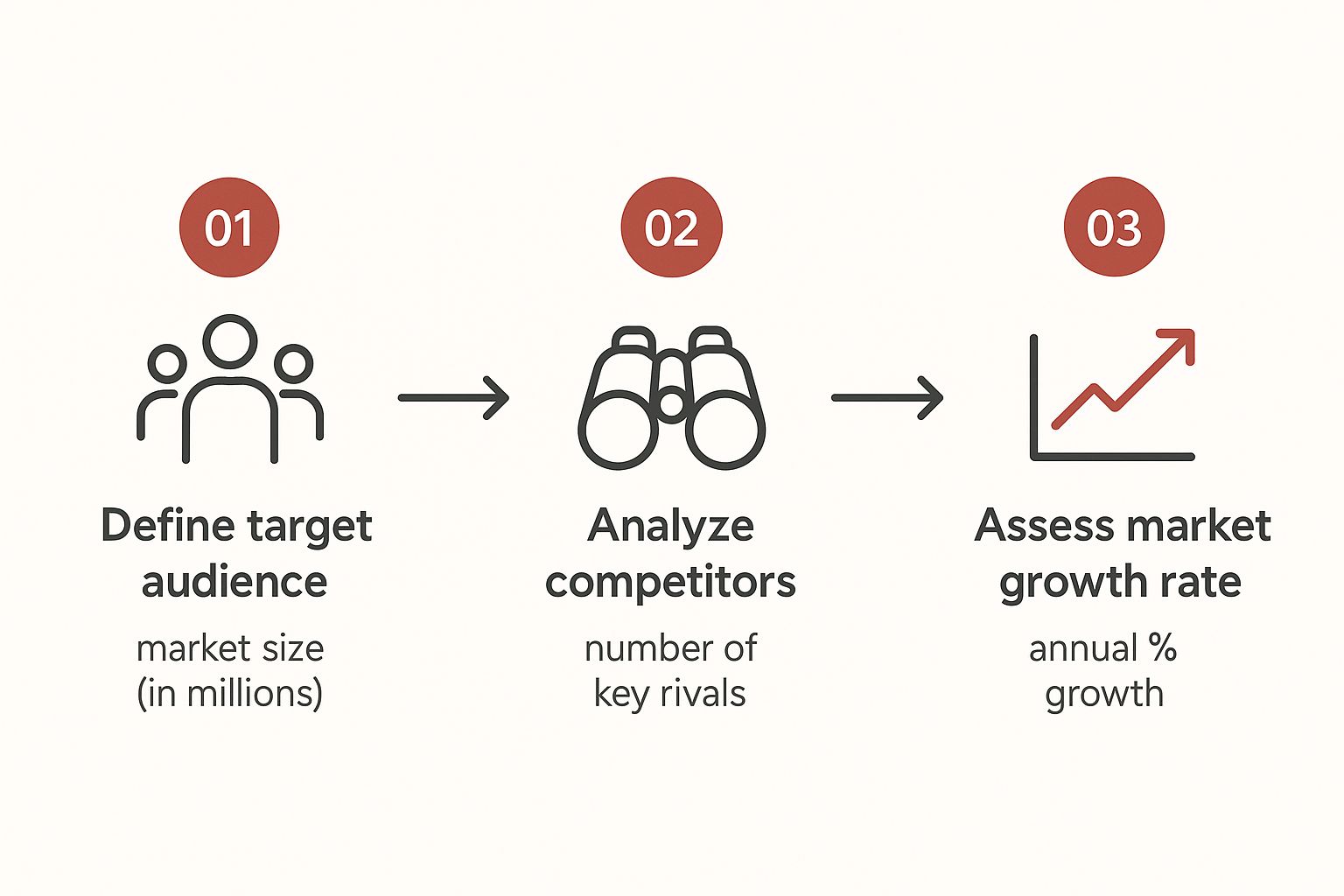

Before you even get to prioritizing features, however, you need to have a rock-solid understanding of the market. The infographic below shows how defining your audience and analyzing the competition sets the stage for everything that follows.

This process isn't just a box-ticking exercise. It's the foundation that ensures your MVP features are a direct response to a genuine market need.

Building What Truly Matters First

With your priorities straight, you can create a focused scope for your MVP. This isn't just a list for your developers; it's your strategic blueprint for launch.

To finalize your MVP scope, you need to answer these questions with absolute clarity:

- Who is this for? Be laser-focused. You aren’t building for "everyone." You're building for that specific person you identified during your validation phase.

- What is their #1 problem? Your MVP must solve this single problem incredibly well. Don't try to solve three problems poorly.

- What is the core user journey? Map out the bare-minimum steps a user needs to take to get value. For example: Sign up -> Search for a chicken recipe -> View ingredients and instructions. Anything outside this essential path can wait.

And remember, the "V" in MVP stands for viable. A product that crashes, looks unprofessional, or is confusing is not viable, no matter how minimal it is. You must deliver a high-quality experience within your limited feature set. Your first users are your most valuable source of feedback, and a clunky, frustrating product will send them running before they can ever tell you what you need to hear.

Let's Talk Money: A Founder's Guide to Startup Funding

So, you've built and validated your MVP. Awesome. Now the conversation almost inevitably shifts to one thing: money. It’s easy to think of funding as the finish line, but that’s a rookie mistake. Funding isn't the prize; it's just fuel for the engine you're building.

The real challenge is figuring out what kind of fuel your startup actually needs, and when. So many founders I’ve seen chase venture capital (VC) way too early, and it's a surefire way to lose control of your own vision.

The hard truth is that not every great business is built for the VC track, and that's more than okay. Your funding strategy has to fit your business model, not the other way around. Let's walk through the most common paths so you can figure out what makes sense for you.

What Are Your Real Funding Options?

The world of startup capital is massive, with everything from emptying your savings account to landing multi-million dollar checks on the table. Each path comes with its own set of expectations, pressures, and strings attached.

-

Bootstrapping: This is the purest way to build. You fund the business yourself, using personal savings or, even better, revenue from your very first customers. It's tough, but it forces incredible discipline and a laser focus on profitability from day one. You answer to no one but your customers.

-

Friends and Family: This is often the first check a founder gets from someone else. It can be a lifeline, but you absolutely have to treat it like a professional investment. Get the terms in writing. A handshake deal can destroy important relationships if things go sideways.

-

Angel Investors: These are successful individuals who invest their own money into early-stage companies for a piece of the pie (equity). They're usually more flexible than VCs and can offer incredible mentorship alongside the cash. They’ve been there, done that.

-

Venture Capital (VC): VCs are the big leagues. They are professional investors managing massive funds, and they’re hunting for unicorns. They invest in businesses with the potential for explosive growth because they need a massive return, think 10x or more, on their investment. This is only the right path if you're building a company that can genuinely dominate a huge market.

Choosing how to fund your company isn't just about the money. It's one of the most critical strategic decisions you'll make. Bootstrapping gives you 100% control, while taking investor money means you are now accountable for delivering on their expectations for massive growth and an eventual exit.

The global startup ecosystem is humming with activity, and investors are always looking for the next big thing. It's not uncommon for angel investors and VCs to pour millions into companies before they even have paying customers. It's a high-risk, high-reward game. With some regions like Asia-Pacific seeing 27.4% year-over-year expansion, opportunity is everywhere.

How to Craft a Pitch That Actually Lands

No matter who you're talking to, an uncle, an angel, or a top-tier VC, you need a story that connects. Your pitch deck is that story, told in slides. It needs to be clear, compelling, and brutally concise. Forget the fancy graphics; investors want clarity.

Your pitch has to nail these fundamental questions, leaving no room for doubt:

- The Problem: What real-world pain are you solving? Make the investor feel it. If you can put a number on how much that pain costs people or businesses, even better.

- Your Solution: How, exactly, do you make the pain go away? Show them what makes your approach different and better than anything else out there.

- The Market: How big is this playground? Investors need to see that the total addressable market is large enough to build a massive company.

- Your Business Model: Straight up, how do you make money? Get specific on pricing, who pays, and how the revenue streams work.

- The Team: Why you? Why this team? You need to sell them on the idea that you are the only people on the planet who can pull this off. Showcase your unique experience.

- The Ask: How much money do you need, and what are you going to do with it? Don’t just ask for a pile of cash. Show them exactly how their capital gets you to the next set of critical milestones.

Remember, investors sit through hundreds of these pitches. Yours has to cut through the noise by being direct and, most importantly, backed by the evidence you gathered during your validation and MVP stages. This isn't about selling a cool idea anymore. It's about proving you have a rock-solid plan to build a valuable company.

Getting the Ball Rolling: Your Launch and First 100 Users

Alright, your MVP is built. Now the real fun begins. Launching a product without a strategy is like throwing a party and not sending out any invitations. You have to switch gears from being a builder to a marketer, and your first mission is a big one: find and win over your first 100 users.

This initial cohort is pure gold. They're not just a number on a dashboard; they’re your first real-world focus group, your future case studies, and, if you play your cards right, your most vocal champions. The secret is to stop thinking about "marketing" and start thinking about finding people where they already hang out.

Go Where Your Customers Live Online

Forget about dumping money into ads or blasting out generic emails. In these early days, your plan of attack needs to be precise, personal, and often, completely free. Your job is to become a helpful, known presence in the online communities your ideal customers already trust.

This means you’ll be spending a lot of time in places like:

- Niche Subreddits: Dig into Reddit to find the communities where people are actively complaining about the very problem you solve. Don’t just spam your link. Join conversations, offer real advice, and only bring up your product when it's genuinely the perfect solution to someone's question.

- LinkedIn & Facebook Groups: Just like Reddit, these groups can be a goldmine. Share what you know, answer questions, and build a bit of a reputation. People are far more likely to check out a product from someone they see as a helpful expert.

- Industry Forums & Slack Channels: If you're building for a specific professional crowd, you need to be in their private forums or Slack groups. Becoming a trusted voice there is worth more than any ad campaign you could run.

This hand-to-hand combat approach doesn't scale. That’s the entire point. At this stage, it’s not about volume; it’s about quality. You’re not just collecting sign-ups; you’re building relationships and getting priceless feedback directly from the people you want to serve.

Your first 100 users won't come from a slick marketing hack. They'll come from you personally showing up, being genuinely helpful, and inviting them to try something you poured your heart into building for them.

Create Content That Pulls People In

While you're engaging in communities, you can also start creating content that acts as a magnet for your ideal users. You don’t need a massive blog with dozens of posts. You just need a few incredibly valuable pieces that solve a specific, nagging problem for your audience.

For example, if your product helps freelance designers manage their projects, a killer blog post would be "The Ultimate Guide to Pricing Your Design Services." It's not a sales pitch. It’s a resource that provides immediate value, which builds trust and attracts the right kind of attention.

This is also where you can plant the seeds for long-term growth. Getting a handle on search engine optimization from day one gives you a massive advantage down the road. You can learn more about what search engine optimization is and see how it helps people discover you organically.

Once you have that killer piece of content, put it to work. Share it in those communities you’re active in, use it to answer questions on sites like Quora, and make it a cornerstone of your early outreach.

You Can't Improve What You Don't Measure: Set Up Analytics Now

This last part is an absolute must-do. It’s so easy to get swept up in the excitement of the launch and think, "I'll deal with data later." That’s a huge mistake. You need to see what's happening from the moment your very first visitor lands on your site.

Setting up free, straightforward tools like Google Analytics is non-negotiable. You don't need a Ph.D. in data science, but you absolutely need to track a few critical things:

- Acquisition: Where are people coming from? This shows you which of your community efforts are actually paying off.

- Behavior: What are they doing once they sign up? Are they using that key feature you built? Where do they get stuck and leave?

- Retention: Are they coming back? Seeing people return is one of the earliest and strongest signals that you might be onto something real.

This early data isn't about hockey-stick growth charts. It's about learning. It gives you the concrete insights needed to have smarter conversations with your users and make informed decisions about what to fix or build next. Without it, you're just guessing.

Assembling Your Founding Team and Culture

Here's a hard truth: the most important thing you’ll ever build isn't your product. It’s the team of people who build that product. Getting your founding team right is a make-or-break moment that dictates your company's entire future. A bad hire early on is like a slow-acting poison, while the right ones are a genuine force multiplier.

Your first few hires, especially a co-founder, are about so much more than just plugging a skill gap. You need to find people who share your vision and, even more critically, your resilience. A slick resume is great, but true grit and adaptability are the traits that will drag a company through the inevitable tough times ahead.

Finding the Right Co-Founders

Choosing a co-founder is a lot like choosing a spouse. A bad partnership can lead to a messy, expensive, and emotionally draining divorce for the business. You need someone with complementary skills who you can trust without a second thought. If you're the tech wizard, you need to find someone who lives and breathes sales and marketing.

Look past the skills and really evaluate their character. Have they ever failed at something big? How did they react? How do they handle intense pressure? The answers to these questions are the real indicators of a strong partner.

Don't underestimate the power of experience, either. First-time founders see an 18% success rate, but that number jumps to around 30% for founders who have successfully built a company before. That leap isn't magic; it comes from the invaluable, often painful, lessons learned from past ventures. You can dig deeper into how experience impacts startup outcomes to see just how much of an edge it provides.

Your first ten employees set the cultural DNA for your first one hundred. Hire for values and attitude over pure experience every time. You can teach skills, but you can't teach character.

Building a Healthy Culture from Day One

Company culture isn’t about ping-pong tables or a fridge full of free snacks. It's the unwritten rules for how your team works together, makes decisions, and treats each other when the pressure is on. As the founder, you are the one setting that tone from the very beginning.

To create a strong foundation, get everyone on the same page from day one.

- Define Clear Roles: Actually write down who is responsible for what. Ambiguity breeds conflict, especially when things get stressful.

- Create a Founder Agreement: This is a non-negotiable legal document that outlines ownership, roles, and what happens if someone decides to leave. It prevents absolute disasters down the line.

- Align Incentives: Use equity to give your earliest team members a real stake in the company's success. This gets everyone’s financial interests pointed in the same direction and fosters a powerful sense of ownership.

When you're intentional about your people and your culture, you transform a common point of failure into your single greatest asset for the long journey ahead.

Common Questions About Building a Startup

Once your idea starts feeling like a real business, a whole new set of practical questions will inevitably creep in. These are the nitty-gritty details that can keep a founder up at night, so let's tackle a few of the most common ones head-on.

One of the first questions is almost always about money: "How much funding do I really need?" The honest answer? As little as possible to hit your next big milestone.

Don't just pull a huge number out of thin air. Instead, build a simple, bottom-up budget. Tally up your essential costs for the next six months, things like basic software, incorporation fees, and a small budget for that first marketing test.

Your goal isn't to build a massive war chest. It's to get just enough cash to prove your next assumption, whether that's landing your first 100 users or confirming your pricing model works. This lean approach forces discipline and makes your "ask" far more credible when you do talk to investors.

Navigating Key Founder Decisions

Another big one I hear all the time is about when to finally quit your day job. This is a deeply personal decision, but my advice is to wait until your startup shows real, concrete signs of life.

What does that look like? It could be a few different things:

- Consistent Revenue: Your side hustle is bringing in enough cash each month to cover your basic living expenses.

- Strong User Growth: You aren't profitable yet, but your user base is growing at a predictable, encouraging rate week after week.

- Significant Funding: You've successfully closed a funding round, giving you a clear runway to pay yourself a modest salary.

Don't quit your job on passion alone. Wait for the data to tell you it's the right time. A steady paycheck in the early days keeps personal stress down, which helps you make clearer, more strategic decisions for the business.

Finally, let's talk about protecting your intellectual property (IP). So many first-time founders are terrified someone will steal their brilliant idea. It's a valid thought, but in the early days, execution is what truly matters, not the idea itself. The best protection you have is speed and building a base of customers who love what you do.

That said, taking a few basic steps is just smart. Look into filing a trademark for your brand name and logo. And if you're sharing sensitive details, make sure anyone you work with signs a non-disclosure agreement (NDA). These simple measures give you a foundational layer of security without getting you stuck in expensive legal battles before you even have a product.

At Digital Lotus Marketing, we specialize in helping startups build a solid foundation for growth. From crafting a compelling brand to running targeted SEO strategies that bring in your first customers, we provide the expert guidance you need to make your mark. Build your startup's marketing plan with us today.